SpaceX: Just Late Stage Goldrush Things

Commentators babbling about Elon's "Amazing UJSD 950M infrastructure deal", don't seem to have read the actual deal.

Here's the summary:

SpaceX, having failed to strike gold, is now forced to rent out the shovels it bought at tremendous markup during the early stages of the gold rush to it's competitors, some of whom (Anthropic) actually struck gold.

This is an excellent deal for Google and a show of how badly SpaceX is doing overall:

Google is a SpaceX competitor and also an investor standing ready to gain double to triple digit billions from their IPO.

Like Google, SpaceX is pursuing vertical integration to ensure value is captured along the chain - Services, LLM, compute, but unlike Google, they don’t have TPU, meaning they have to buy all Nvidia for compute.

That’s a huge issue for SpaceX because Nvdia’s profit margins (75+%) are the primary (!) thing that makes AI expensive. GPU DCs are costly to build and most of the hardware depreciates over 3-5 years. To start making a profit (margins about 20%, not exactly great for this class of companies), your GPU utilization has to be high, 65-70%:

❓Why is this a great deal for Google?

We are several years into the bubble and the expectations are sky high. Whoever is at the AI CapEx poker table is all in and players have started tendering equity or issuing bonds to stay in the game^1.

There’s two scenarios that companies are worried about:

1. Demand rises massively and they can’t capture the wins because lead times are long.

2. Demand crashes and they have to write off massive infrastructure investments. TPU or not, the supply crunch has made investments in future compute very expensive.

This deal acts as a hedge for Google:

If demand skyrockets, prices for Nvidia compute will too and Google just secured access to a lot of top end compute at a rate that will be very reasonable under demand pressure.

If the bubble bursts, demand craters or stays flat, SpaceX will have to write off the Capex because google has the contractual rights to just cancel the deal.

Tech companies fear missing out on growth more than writing down investments, because the risk for the second is covered by investors

SpaceX has the same, but unlike Google, they have no credible claims on any gold to shovel with the compute.

❗The upside here goes to Google, majority of the risk to SpaceX. For SpaceX, selling raw compute to competitors is the lowest margin play:

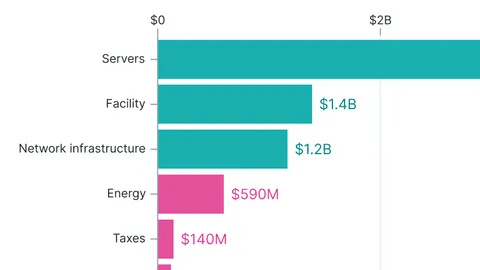

Colossus was built to train Grok and serve other xAI plays on their on their compute. As a rushed fossil powered DC with a high failure rate on GPUs it’s not very competitive on the overall compute market.

The lopsided deal shows these plays have failed, we know from industry reporting that before the Anthropic deal, Collosus I only had about 11% of utilization^2, depreciating hundreds of millions, if not billions of dollars a month on top of training expenses in the hundreds of millions for Grok^3 which has failed to get any traction.

The PR effect of “SpaceX gets (up to) 900M from Google a month (cancellable on short notice)” is cherry on top juicing IPO narrative.

The rules are simple:

If you struck gold and renting shovels is faster then buying or building them, rent to extract as much gold as possible before your competitors (Anthropic)

If there's a chance you may strike gold, renting shovel options is a lower risk play, since shovels will become more expensive when gold is found (Google)

If you have a stake in a shovel vendor about to IPO, loudly proclaim you're buying shovel options, trusting the media to mistake options for commitment (Everyone in AI)

^1: [https://www.msn.com/en-us/money/top-stocks/alphabet-stock-drops-as-80b-ai-fundraising-plan-shakes-wall-street/ar-AA24EyBl]

^2: https://wccftech.com/xai-using-just-11-percent-gpus-while-meta-google-squeeze-out-much-more/

This is an excellent deal for Google and a show of how badly SpaceX is doing overall: Google is a SpaceX competitor and also an investor standing ready to gain double to triple digit billions from… | Georg Zoeller | 13 comments

Commentators babbling about Elon's "Amazing UJSD 950M infrastructure deal", don't seem to have read the actual deal. Here's the summary: ==SpaceX, having failed to strike gold, is now forced to rent out the shovels it bought at tremendous markup during the early stages of the gold rush to it's competitors, some of whom (Anthropic) actually struck gold.== This is an excellent deal for Google and a show of how badly SpaceX is doing overall: Google is a SpaceX competitor and also an investor standing ready to gain double to triple digit billions from their IPO. Like Google, SpaceX is pursuing vertical integration to ensure value is captured along the chain - Services, LLM, compute, but unlike Google, they don’t have TPU, meaning they have to buy all Nvidia for compute. That’s a huge issue for SpaceX because Nvdia’s profit margins (75+%) are the primary (!) thing that makes AI expensive. GPU DCs are costly to build and most of the hardware depreciates over 3-5 years. To start making a profit (margins about 20%, not exactly great for this class of companies), your GPU utilization has to be high, 65-70%: ❓Why is this a great deal for Google? We are several years into the bubble and the expectations are sky high. Whoever is at the AI CapEx poker table is all in and players have started tendering equity or issuing bonds to stay in the game^1. There’s two scenarios that companies are worried about: 1. Demand rises massively and they can’t capture the wins because lead times are long. 2. Demand crashes and they have to write off massive infrastructure investments. TPU or not, the supply crunch has made investments in future compute very expensive. This deal acts as a hedge for Google: If demand skyrockets, prices for Nvidia compute will too and Google just secured access to a lot of top end compute at a rate that will be very reasonable under demand pressure. If the bubble bursts, demand craters or stays flat, SpaceX will have to write off the Capex because google has the contractual rights to just cancel the deal. {{attachment:spacex.jpg}} ==Tech companies fear missing out on growth more than writing down investments, because the risk for the second is covered by investors== SpaceX has the same, but unlike Google, they have no credible claims on any gold to shovel with the compute. ❗The upside here goes to Google, majority of the risk to SpaceX. For SpaceX, selling raw compute to competitors is the lowest margin play: Colossus was built to train Grok and serve other xAI plays on their on their compute. As a rushed fossil powered DC with a high failure rate on GPUs it’s not very competitive on the overall compute market. The lopsided deal shows these plays have failed, we know from industry reporting that before the Anthropic deal, Collosus I only had about 11% of utilization^2, depreciating hundreds of millions, if not billions of dollars a month on top of training expenses in the hundreds of millions for Grok^3 which has failed to get any traction. The PR effect of “SpaceX gets (up to) 900M from Google a month (cancellable on short notice)” is cherry on top juicing IPO narrative. The rules are simple: ==If you struck gold and renting shovels is faster then buying or building them, rent to extract as much gold as possible before your competitors (Anthropic)== ==If there's a chance you may strike gold, renting shovel options is a lower risk play, since shovels will become more expensive when gold is found== (Google) ==If you have a stake in a shovel vendor about to IPO, loudly proclaim you're buying shovel options, trusting the media to mistake options for commitment== (Everyone in AI) ^1: [https://www.msn.com/en-us/money/top-stocks/alphabet-stock-drops-as-80b-ai-fundraising-plan-shakes-wall-street/ar-AA24EyBl] ^2: [https://wccftech.com/xai-using-just-11-percent-gpus-while-meta-google-squeeze-out-much-more/](https://wccftech.com/xai-using-just-11-percent-gpus-while-meta-google-squeeze-out-much-more/) ^3: [Grok itself wasn't cheap. 400M for the final training run for 3.5, which nobody used but XAI on X (a pure loss leader since X ad revenue has cratered) because Claude had a better model within 2 weeks of release, and 500M for Grok 4](https://epoch.ai/data-insights/grok-4-training-resources)

linkedin.com

linkedin.com